So you’ve got an LLC or sole proprietor and you’ve been hearing the term “s-corp” being thrown around online as a way to save on taxes? But a quick Google search of “should I change my business to an s-corp” quickly revealed that the answer isn’t clear-cut or simple.

Generic advice on the internet is dangerous for this reason, but the fact that you’re looking for tax strategies is a good sign! It means your business has been profitable enough that you’re feeling the pain of paying taxes on all that profit. And one way to potentially reduce your the tax burden is to stop paying income taxes on all your business’s profit as a disregarded or pass-through entity. (If these terms are unfamiliar to you, read this short article about pass-through entities to catch up.)

There were advantages to the pass-through model in the business’s early days, but now you’re beginning to wonder if an s-corp election might be the way around paying that ~15.3% self-employment tax on the income your growing business generates. The short answer is YES! Here’s how…

From Disregarded Entity to S-Corp (What Changes and Why)

If you’re a growth-stage business owner (typically 2–5 years in and consistently profitable) or if you own an established business (typically 5+ years of consistent revenues), pass-through taxation starts to feel much more expensive.

That’s usually the moment S-corp elections enter the conversation.

Here’s why.

As a sole proprietor or an LLC owner (single or multi-owner), your business is considered a “disregarded entity.” That means 100% of your business’s profit passes through as income to you. That income is subject to:

- Self-employment tax AND

- Income tax

As far as the IRS is concerned, there is no distinction between:

- Money you earned and

- Money you took home

This means that even if you left money in the business in 2026 to invest in growth initiatives in 2027, you’ll pay self-employment and income tax on that profit as if you paid it to yourself. Even though you didn’t.

That may work fine early on in the startup days. But as profits increase, so does the tax burden. That’s when the question of S-Corp vs. LLC taxation starts to become easier to answer.

One quick note – You can’t elect s-corp if you’re a sole proprietor, but you can easily convert your sole prop to an LLC and then elect s-corp status.

First, What is an S-Corp?

I often hear people saying, “I want to open an s-corp” or “I’m ready to convert my LLC to an s-corp.” Believing an s-corp is a type of business (or business entity type) is a common misconception.

An s corporation is not a business entity. You can’t “open an s-corp” business. It’s a tax election status.

You can elect “s-corp” tax status by following a few careful steps. But the status isn’t just a box to be checked; there are requirements you must meet both to take advantage of the status and to fulfill the IRS’s requirements.

For this reason, electing s-corp status requires forward-planning, preferably as early in the year as possible (though you can do a late s-corp election for the prior year with the help of a trusted tax preparer or CPA — reach out for our professional assessment).

Even if you aren’t yet sure if s-corp is right for you, keep reading to learn about it so you’re primed to elect BEFORE you need it instead of after.

How Pass-Through Income Changes When You’re Ready for an S-Corp

What an S-Corp Election Actually Does

An S-corp is not a different type of business — it’s a tax election.

Your business is still a pass-through entity, but the way income flows changes:

✔ You will pay yourself a reasonable salary (subject to payroll taxes)

✔ Remaining profit is taken as distributions

✔ Distributions are not subject to self-employment tax

This doesn’t eliminate taxes — but it can reduce how much income is exposed to payroll taxes.

Why S-Corp Election Timing Matters

An S-corp election makes sense only when:

Profits are high enough to offset the added costs of fulfilling s-corp requirements

You’re ready for payroll compliance

You want more intentional control over tax exposure

This is why the move often happens after the first few years or after reaching a certain profitability (aka tax pain point).

Early stage = simplicity

Growth stage = optimization

The “S-Corp Signal” for Growth-Stage Owners

If pass-through income is starting to feel painful, that’s not a failure — it’s a signal. It usually means your business has grown to the point where:

- Structure matters

- Payroll becomes strategic

- Tax planning shifts from defensive to proactive

And that’s exactly where growth-stage tax strategy begins.

Visual Metaphor: “The Bucket vs. The Funnel”

This is a metaphor we often use when helping our small business owner clients decide when to elect s-corp status:

Pass-Through Entity = One Big Bucket

Imagine your business income pouring into one large bucket.

Every dollar that lands in the bucket:

- Is treated as your income

- Is fully exposed to income + self-employment tax

You can scoop money out (pay yourself) or leave it in — but the tax exposure doesn’t change.

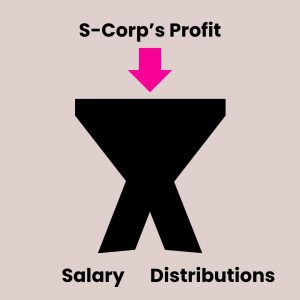

S-Corp = A Funnel with Two Streams

Now imagine that same income flowing through a funnel:

💰 Stream 1: Salary (taxed as normal wages)

💰 Stream 2: Distributions (not subject to self-employment tax)

Same income. Different flow. More control.

Early on, one bucket is fine — simple and efficient. As income grows, a funnel gives you options. And tax strategy is really about this: Not changing how much you earn — but changing how income flows.

What S-Corp Election Looks Like in Real Life: $150,000 Profit, Two Different Tax Outcomes

Let’s walk through a simplified example to show why pass-through taxation can start to feel painful as profits grow — and how an S-corp election can change the math.

⚠️ Important note: These numbers are approximate and meant to illustrate how the mechanics could work, not to calculate an exact tax bill.

Scenario 1: Pass-Through Business (Sole Proprietor or LLC)

Your business profits $150,000 for the year. Because your business is a pass-through entity, the entire $150,000 is treated as your personal income. Contact an experienced tax preparer to calculate your potential tax scenarios.

It is subject to:

- Income tax and

- Self-employment tax (15.3%)

Self-Employment Tax Calculation:

$150,000 × 15.3% = $22,950

That $22,950 covers:

- Social Security

- Medicare

And it applies whether you actually pay yourself all that money or save some in the business bank account for a rainy day.

Income Tax (Simplified)

Let’s assume an effective combined federal/state income tax rate of 22%:

$150,000 × 22% = $33,000

Total Estimated Taxes for Pass-Through Entity Income

Self-employment tax: $22,950

Income tax: $33,000

👉 Total taxes due: $55,950

Scenario 2: Same Business, S-Corp Election

Now let’s look at the same business, same $150,000 in profit — but structured as an S-corp.

You pay yourself:

- $75,000 salary

- $75,000 distributions

Payroll Taxes on Salary Portion

Your salary is subject to payroll taxes (Social Security + Medicare):

$75,000 × 15.3% = $11,475

This payroll tax is split:

- Half paid by the company

- Half withheld from your paycheck

Economically, it’s still part of the overall tax cost of running the business.

Federal Income Tax on Total Earnings

You still pay income tax on:

- Your salary and

- Your distributions

Using the same simplified 22% effective rate:

$150,000 × 22% = $33,000

Total Estimated Taxes (S-Corp)

Payroll taxes on salary: $11,475

Income tax: $33,000

👉 Total: $44,475 in taxes

Side-by-Side Comparison: Pass-Through vs. S-Corp Election

Estimated Total Taxes:

Pass-through (LLC/Sole Prop) $55,950

S-corp election $44,475

Estimated difference:

👉 $11,475 in tax savings

Understanding the Above Example of S-Corp vs. LLC Taxation

Nothing magical happened here.

- The business didn’t earn more money

- No loopholes were used

- No aggressive strategies were applied

The difference came from how income flowed — not how much was earned. That’s why S-corps become a real conversation at the growth stage.

But It’s Not All About Tax Savings: Other S-Corp Factors to Weigh

An S-corp is not automatically better. You also need to consider:

- Payroll processing setup and management headache

- Costs to setup and run payroll

- Additional compliance

- State-specific s-corp/franchise fees (fees in states like California or New York may offset tax benefits for businesses with profits under $60k)

- How to comply with reasonable salary requirements, which are not straightforward (typical IRS)

This is why timing matters — and why S-corps tend to make sense after profits are consistently strong, not in the first year. If your first year is gangbusters but the second year takes a big dip (not uncommon), your salary could put

The Bottom Line

If your business is consistently profiting six figures or more, pass-through taxation can quietly cost you tens of thousands of dollars over time.

An S-corp doesn’t eliminate taxes — but it can give you more control over how much income is exposed to payroll taxes.

And that’s often the difference between growing comfortably — and growing with friction.

Thinking you might be ready for an s-corp election. The first step is ensuring your books are organized and complete, so you have accurate financial data to make your decision. If your books have been neglected or you aren’t sure they’re correct, you’re in the right place for a books cleanup. Our Cleanup Queen will have your books in ship-shape form so you can quickly make an informed decision about electing s-corp.

Book a a free consult or click here to learn more about our bookkeeping cleanups.

If you already have accurate, up-to-date accounting and you think you can save by electing s-corp, there’s no time to waste. Contact us and we’ll help you elect s-corp and set up the payroll required for s-corp elections.

Gutsy Money: When it comes to strategic tax efficiency, we’ve got your back!